Plan Special Needs founder Jitendra P.S. Solanki is a Chartered Trust and Estate Planner and a Fiduciary fee only financial planner. He has gained a deep understanding into special needs children families’ personal, financial and legal requirements. This helps in understanding the trust provisions to be created and what difficulties can arise in future while forming the trust. Also, In most of the special needs trust parents are the initial trustees. Not well versed with trust affairs they face difficulties in understanding and managing trust. For Trusts, not funded with large corpus, appointing a professional trustee may be a costly option for the parents. With our expertise we have launched support services to such trusts so that parents and future trustees can manage the trust affairs more efficiently.

Right from the creation of special child trust to becoming a professional trustees we have launched wide variety of services to Special Needs Child Trust.

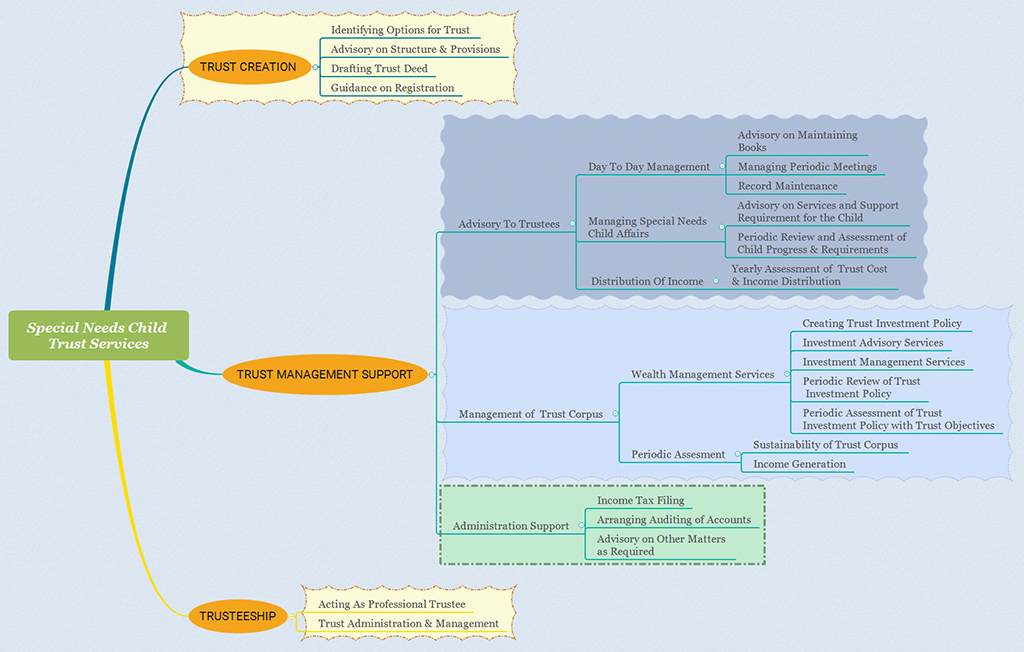

Our list of services includes :

- Advisory On Trust Creation – It involves pre-discussion on assessing the viability of trust formation for special needs child life long care.

- Support In Trust Management – Here we support the trustees in managing the trust. The support services includes Guidance in understanding special needs child requirement, day to day management, conducting trustee meetings, maintaining records, analysing the sustainability of trust corpus, managing trust corpus, and others as illustrated in below chart.

- Trusteeship Services – Jitendra P.S. Solanki works as a professional trustee in individual capacity. The benefit of appointing him a professional trustee is that he works in a Fiduciary capacity who will stand in a position of trust with you (or your estate after your death) and your beneficiaries. Moreover, he is well aware of the trust management for special needs child lifelong care.

All the above services are on fee basis which will depend on the scope of work involved.

To get more details on the above services write to us: